Closing is the final step in homeownership where ownership legally transfers to the buyer. Learn how to prepare for a smooth closing process.

Closing is the final step in homeownership where the property officially transfers to the buyer.

What is Closing?

Closing, sometimes called settlement, is the stage where everything comes together in your homeownership journey. It’s the point when the buyer, seller, and other parties finalize their obligations, ensuring the sales contract is complete. Most importantly, closing is when ownership of the property legally transfers to the buyer. In other words, it’s the final milestone where the keys to your new home are officially yours.

Why the Closing Process Matters

Closing is much more than a signature—it’s the safeguard that ensures every financial and legal detail is in place. From reviewing mortgage documents to confirming payments and recording the deed, this step ensures a seamless transfer of ownership. Without a smooth closing, you risk unnecessary delays, financial setbacks, or even contract cancellations.

How to Prepare for Closing

Being ready for closing is all about organization and timing. Here are a few essentials to keep in mind:

Review documents early: Request your closing disclosure at least three business days prior. Bring required funds: Ensure you have your cashier’s check or wire transfer prepared. Verify identification: Bring a government-issued photo ID for signing documents. Do a final walkthrough: Confirm the property is in agreed-upon condition before signing.

By preparing ahead, you’ll minimize stress and enjoy a smoother transition into your new home.

Closing: The Key Moment in Homeownership

The closing process represents the finish line of your real estate journey. After weeks or even months of searching, negotiating, and securing financing, this final step unlocks your dream home. Whether it’s your first home or an investment property, closing solidifies your role as the new homeowner.

If you’re getting ready to buy, don’t go through closing alone. Let me guide you through each step, ensure your mortgage options are aligned with your goals, and celebrate with you as you receive the keys to your new home.

Buyers today prioritize environmentally friendly home features like energy-efficient appliances, HVAC, and lighting. Learn how going green boosts comfort, savings, and value.

Discover environmentally friendly home features buyers consider very important for savings, comfort, and home value.

Environmentally Friendly Home Features Buyers Value Most

Going green is no longer just a lifestyle choice—it’s a smart financial move. Today’s homebuyers are prioritizing environmentally friendly home features that combine comfort, efficiency, and sustainability. From lowering utility bills to increasing resale value, these upgrades make homes more attractive and future-proof.

The National Association of Realtors (NAR) reports that buyers now consider eco-friendly updates “very important” when searching for their dream home. Features like energy-efficient HVAC systems, updated appliances, insulated windows, and modern lighting aren’t just nice-to-have—they’re game changers.

Heating and Cooling Upgrades

Efficient heating and cooling systems remain at the top of the list. Buyers know outdated HVAC units can drive up monthly costs. By contrast, ENERGY STAR® rated systems keep homes comfortable while cutting energy bills. For sellers, this is a high-impact upgrade that boosts buyer confidence.

Energy Efficient Appliances

Appliances aren’t just about convenience anymore—they’re about long-term savings. Dishwashers, refrigerators, and washing machines that use less water and electricity have become key decision-making factors for eco-conscious buyers.

Windows, Doors, and Siding

Insulated windows and doors aren’t just stylish—they prevent heat loss and keep utility bills manageable. High-quality siding also helps regulate indoor temperatures while protecting the home from weather damage.

Energy Efficient Lighting

LED lighting has become an essential upgrade. Homebuyers appreciate homes already equipped with modern lighting that consumes less electricity and lasts longer. It’s a small feature with a big impact.

Why It Matters for Buyers and Sellers

Eco-friendly features aren’t just trends—they’re investments. For buyers, they translate into long-term savings and comfort. For sellers, they mean a stronger selling point and potentially higher offers. Even better, some mortgage and refinance programs offer incentives for eco-conscious homes, making it easier to qualify for competitive rates.

If you’re curious about qualifying for an energy-efficient mortgage (EEM) or learning how your home’s green features could save you money, now’s the time to explore your options.

Budgeting for a home doesn’t have to be stressful. Discover how to plan your loan, payments, and future with clarity and confidence.

Image Caption: Budgeting for a home—clarity, confidence, and smart financial planning.

A pink-themed graphic with bold purple icons of a dollar sign, multiplication sign, and division sign. The text reads “Budgeting For a Home? Let’s Do The Math!” followed by supportive messaging about guiding homebuyers through loan programs and monthly payments with clarity and confidence.

Understanding Budgeting for a Home

Buying a home is one of life’s most exciting milestones—but it can also feel overwhelming when it comes to the financial side of things. That’s why budgeting for a home is not just about crunching numbers, it’s about creating peace of mind. From estimating your monthly mortgage payments to choosing the right loan program, knowing your numbers gives you the confidence to move forward.

Instead of guessing, you can work with a trusted loan professional who breaks everything down into simple, easy-to-follow steps. That way, you’ll understand what fits comfortably into your budget while keeping your long-term financial goals intact.

Loan Programs Made Simple

Not all loans are created equal. FHA, VA, USDA, and conventional loans each come with different requirements, benefits, and payment structures. Choosing the right one depends on your income, credit score, and how much you can comfortably put down. A good loan officer will not only explain your options but also help you see which program supports your unique financial situation.

When budgeting for a home, this guidance is invaluable. Instead of uncertainty, you get clarity—and instead of stress, you gain confidence.

Monthly Payments and Long-Term Planning

Understanding your monthly payments is at the heart of successful budgeting. These payments include more than just principal and interest. You also need to consider taxes, homeowners insurance, and possibly private mortgage insurance (PMI). Factoring in all these costs upfront prevents surprises later.

The goal isn’t just to buy a home—it’s to stay in your home comfortably, without stretching your budget too thin. By planning carefully, you’ll know exactly what your financial future looks like, making your dream home feel truly attainable.

Why Clarity and Confidence Matter

The real win in budgeting for a home isn’t simply qualifying for a mortgage—it’s knowing that you’re making the best financial decision for yourself and your family. With the right guidance, you’ll feel confident every step of the way, from pre-approval to closing day.

So, are you ready to do the math together? Let’s take the guesswork out of buying your dream home. Send me a message today, and let’s make a plan that works for you.

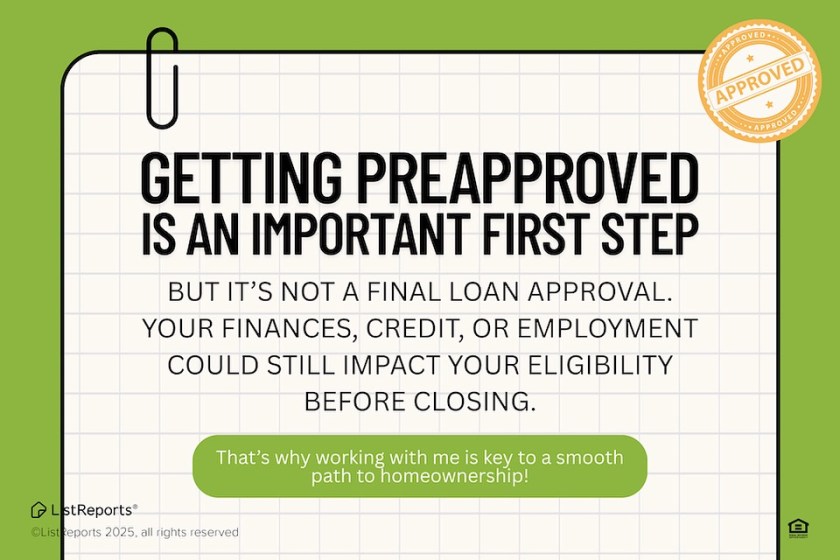

Getting preapproved is an important first step in buying a home, but it’s not final approval. Learn what happens next and how to protect your eligibility.

Getting preapproved is a vital first step, but it’s not a final loan approval—your finances still matter before closing.

Getting Preapproved Is Just the Beginning

Getting preapproved is exciting 🎉—it means a lender has reviewed your basic financial information and believes you could qualify for a mortgage. But here’s the thing: preapproval is not the final green light. Before you get the keys to your dream home, your finances, credit score, and employment status will still be reviewed again. Any major changes could impact your eligibility before closing.

Why Preapproval Matters

Preapproval shows sellers you’re serious and financially prepared. It can make your offer stand out in a competitive market and give you a clear idea of your budget. However, this first step is just that—a step. The final loan approval happens only after your lender verifies all details through underwriting.

How to Protect Your Preapproval

To avoid surprises at closing, here are a few tips:

Keep your credit stable – avoid new debt or big purchases before closing. Maintain employment – lenders will confirm your job status before final approval. Stay financially consistent – large, unexplained bank deposits or withdrawals can raise questions.

Your Trusted Guide from Start to Finish

That’s why working with a knowledgeable loan officer is essential. I’ll help you understand what’s expected at every stage so you can avoid pitfalls and close with confidence. From the day you get preapproved to the moment you hold your keys, I’ll be by your side to make the journey as smooth as possible.

Ready to take the first step toward homeownership?

Learn what net proceeds are, why they matter when selling your home, and how to calculate them so you can plan your next move with confidence.

Understanding your net proceeds helps you know exactly what you’ll walk away with after selling your home.

What Are Net Proceeds in Real Estate?

When you sell your home, the final amount you actually get to keep isn’t the same as your sale price. Net proceeds are the true bottom-line figure—the amount you walk away with after subtracting all mortgages, liens, and selling costs. These expenses often include:

Mortgage payoffs Real estate agent commissions Closing costs Any outstanding liens Repairs or concessions to the buyer

Why Net Proceeds Matter for Home Sellers

Your net proceeds determine what you have available for your next purchase, paying off debt, or investing elsewhere. Many homeowners focus on their listing price but forget to factor in these deductions. This can lead to unrealistic expectations—and possibly frustration—when the final check is smaller than imagined.

By calculating your net proceeds early, you gain clarity and can make smarter financial decisions. It’s the number that helps you:

Set realistic selling goals Budget for your next home purchase Plan for moving costs and other expenses

How to Estimate Your Net Proceeds Before You Sell

You don’t need to wait until closing day to know your number. Working with a real estate or mortgage professional, you can run an estimated net sheet based on:

Your expected sale price Estimated payoff amounts for mortgages or liens Anticipated transaction costs

Want a quick calculation? Try using a trusted online tool like Bankrate’s Net Proceeds Calculator or contact me for a personalized breakdown.

Let’s Calculate Yours Together

Knowing your net proceeds gives you peace of mind and helps you plan confidently. I can walk you through the numbers so there are no surprises on closing day. Curious about your net proceeds? Let’s run the numbers together and make sure you’re ready for your next big move.

Refinancing your mortgage can save you money, reduce debt, or free up cash. Discover how refinancing works and if it’s the right move for you.

What is refinancing? A helpful definition and guide to how it works.

Refinancing Your Mortgage

Refinancing your mortgage simply means replacing your existing home loan with a new one—often with better terms. According to ListReports, refinancing is typically done to lower your interest rate, reduce your monthly payment, or restructure your debt. Sounds good, right? But what’s really behind this savvy financial move?

When you refinance, you essentially take out a new loan to pay off your current one. The new loan could have a lower interest rate, which means you pay less over time. But refinancing isn’t just about savings—it’s about strategy. Whether your goal is to shorten your loan term, cash out some equity, or just lower your bills, refinancing gives you options.

Let’s explore how refinancing can work in your favor and why now might be a great time to act.

Why Refinance?

Lower Interest Rates: A drop in rates can translate into serious long-term savings. Smaller Monthly Payments: Save hundreds annually with a reduced payment. Debt Consolidation: Use your home’s equity to pay off high-interest credit cards. Shorten Your Term: Pay off your mortgage faster and build equity sooner. Cash-Out Refinance: Access funds for renovations, investments, or emergencies.

Is Refinancing Right for You?

Refinancing isn’t one-size-fits-all. It’s best to consider:

Your current interest rate Your credit score How long you plan to stay in your home Closing costs Your financial goals

Pro Tip: Use an online mortgage refinance calculator to crunch the numbers or contact a licensed loan officer to guide you through options.

Next Steps: Let’s Connect!

Every financial situation is unique. If you’re wondering whether refinancing makes sense for you, I’d love to chat and review your options. Let’s look at your goals, current loan terms, and how refinancing might help.

Your dream home is closer than you think! Get mortgage guidance from start to finish. Let’s make it happen together.

Magnify your chances of homeownership – fund your dream home with me and start your journey today.

Your Dream 🏠 Home is Closer Than You Think

Buying a home is more than just scrolling through listings and falling in love with a cozy porch or a modern kitchen. It’s a financial journey—and I’m here to help make it smooth, stress-free, and even exciting. If you’ve been wondering how to fund your dream home, you’ve landed in the right place.

From the moment you start thinking seriously about homeownership, one of the most important relationships you’ll need is with a mortgage expert. I guide you step-by-step through the entire financing process—from getting preapproved, all the way through to signing those final papers at closing.

What I Offer as Your 🦸♂️ Loan Officer

Preapproval guidance to help you know your budget early Flexible loan options tailored to your needs Clear communication so you’re never left in the dark Ongoing support during house hunting Confidence on closing day so you feel secure in your investment

By working together, we’ll turn “For Sale” signs into “Dream Come True” stories—just like the image above promises. 🏡 Whether you’re a first-time buyer or upgrading to a forever home, your vision matters, and I’m here to help bring it to life.

Why 🎬 Start Now?

The real estate market moves fast—and opportunities don’t wait. Whether you’re seeing rates you like, properties that speak to you, or you’re just ready for a change, now is the time to take action. Don’t let confusion or fear stop you. Instead, let me show you how financing your dream home can be simpler than you ever imagined.

Let’s Turn Your Dream Into an Address 🏁

Want to take the first step? Contact me here for a personalized consultation. Let’s talk about your goals, budget, and how we can make your dream home a reality. Already house hunting? Great—get preapproved today and shop with confidence.

Snagging a home this summer doesn’t have to be overwhelming. With a few smart strategies like getting preapproved, considering fixer-uppers, and checking out older listings, you can make your dream of homeownership a reality.

A young family tours a potential new home—ready to snag a home this summer with smart buying tips.

How to Navigate a Hot Market With Strategy and Confidence

Summer is a fantastic time to shop for your dream home, but it’s also when competition heats up. If you’re serious about getting ahead in today’s real estate market, you need more than just desire—you need a plan. From getting preapproved early to exploring homes with hidden potential, smart choices can make all the difference.

Let’s walk through three key strategies that will help you stand out and snag a home this summer before someone else does.

Don’t Wait to Get Preapproved

Getting preapproved should be your first move. It tells sellers you’re serious and financially ready, and it helps you shop within your real budget. Not only does this streamline your search, but it gives you an edge in multiple-offer situations, which are common in summer months.

As a trusted loan officer, I work with clients every day to simplify the preapproval process. If you’re unsure where to start, contact me for a free consultation. We’ll review your finances and help you take this crucial first step confidently.

Consider a Fixer-Upper

It’s tempting to only look at “move-in-ready” homes, but sometimes the best value lies in properties that need a little TLC. A fixer-upper can be a gateway to a better neighborhood, larger home, or even a strong investment if you’re willing to put in some elbow grease.

Talk to your real estate agent or loan advisor about renovation loan options like the FHA 203(k) or HomeStyle Renovation loans. These can help you finance both the purchase and the improvements under one mortgage. Learn more about renovation loans here.

Look at Older Listings

In a hot market, homes that have sat on the market for a while are often overlooked—but that’s where the opportunity lies. Maybe the price was initially too high, or it lacked staging, but these properties can often be negotiated for less, with less competition.

Older listings may also offer flexible closing timelines and sellers who are more open to negotiations or repairs.

Don’t just scroll past a home because it’s been listed for a few weeks. Take a second look—you might find a hidden gem.

Snag a Home This Summer

Whether it’s your first home, a move-up property, or an investment opportunity, the key to success is strategy. This summer, go beyond browsing—take real steps toward ownership by:

Getting preapproved early Being open to homes that need work Revisiting listings others may have ignored

Need help navigating the process? I specialize in helping buyers find the right loan and make confident decisions. Let’s connect today!

Get preapproved faster by gathering these key documents today. Learn how to impress sellers and boost your buying power.

Key documents you need to jumpstart your preapproval process and secure your dream home.

Why Getting Preapproved is a Game Changer for Homebuyers

The homebuying journey can feel like a marathon, but getting preapproved is your secret weapon to starting strong. Before you even step into an open house, a preapproval tells sellers you’re serious—and gives you confidence in your budget. Think of it like showing up with your homework done. The best part? You only need a few simple documents to get rolling.

Let’s face it: buying a home isn’t just emotional—it’s a financial decision. Preapproval helps you set realistic expectations by confirming how much a lender is willing to let you borrow. It gives you the edge in a competitive market where homes are flying off the shelves. So what do you need to make it happen?

Must-Have Documents for Preapproval

✔️ Driver’s License or State ID

This proves your identity. No surprise here—it’s standard practice for any major financial agreement.

✔️ Social Security Number

Used to check your credit and verify your eligibility. Tip: double-check your card to ensure it’s legible and up to date.

✔️ Proof of Income (2 Years)

Lenders want to know you can afford the home. Pay stubs, W-2s, or 1099s will do the trick. Steady income = happy lender.

✔️ List of Current Debts

Got student loans, car payments, or credit cards? Be upfront. Lenders calculate your debt-to-income ratio to decide what you can afford.

The Competitive Edge of Being Preapproved

Imagine walking into a showing and telling the seller: “I’ve already been preapproved.” It’s a power move. Sellers are more likely to accept an offer from someone who’s financially ready to buy. That preapproval letter could be the difference between landing your dream home or losing it to a faster buyer.

Need Help Getting Started?

If all this still feels overwhelming, I’ve got your back. I can connect you with a local loan officer who will walk you through the preapproval process step by step. It’s not just about paperwork—it’s about setting yourself up for long-term success. Send me a message today and let’s talk strategy.

Discover the top environmentally friendly home features buyers consider essential. Boost home value with energy-efficient upgrades today!

Eco-friendly home upgrades like heating, cooling, windows, and lighting attract modern buyers.

Sustainability Is Driving Buyer Decisions in Real Estate

Sustainability isn’t just a passing trend anymore—it’s become a decisive factor in real estate purchases. With eco-conscious buyers actively seeking homes that offer sustainable benefits, prioritizing green features in your property can significantly boost both interest and market value. A recent report from NAR.com, as showcased in the provided infographic, highlights which environmentally friendly features today’s buyers consider “very important” when making home-buying decisions.

From heating and cooling systems to energy-efficient lighting, modern buyers are more aware of their environmental footprint—and they’re willing to invest in homes that help them reduce it.

Heating and Cooling: Essential for Energy-Conscious Buyers

Your home’s heating and cooling systems are not just functional assets—they’re high on the priority list for eco-aware buyers. Upgrading to energy-efficient HVAC systems can reduce energy consumption dramatically, appealing directly to buyers seeking long-term savings and sustainable living. Learn how to optimize your home’s HVAC system in this energy-saving guide.

Why Energy-Efficient Appliances Are Non-Negotiable

Energy-efficient appliances rank just as high in buyer considerations. Modern homeowners appreciate dishwashers, washing machines, and refrigerators designed to minimize electricity usage without compromising performance. Investing in ENERGY STAR-rated appliances is a smart move that signals to buyers your property is both modern and mindful of energy use.

Maximize Insulation with Better Windows, Doors, and Siding

Proper insulation isn’t always visible, but savvy buyers know its importance. New, energy-efficient windows, properly sealed doors, and insulated siding help reduce heating and cooling costs. As illustrated in the infographic, installation upgrades are among the top five features buyers seek. Focus on materials that offer superior thermal insulation and durability to stand out in your market.

Energy-Efficient Lighting: Small Upgrade, Major Impact

While it may seem minor compared to appliances or HVAC systems, switching to LED and other energy-efficient lighting solutions plays a substantial role in home sustainability. Modern buyers look for well-lit homes that won’t spike electricity bills, making this one of the simplest yet most effective upgrades to implement before listing.

How Green Features Increase Your Home’s Market Value

Incorporating environmentally friendly features doesn’t just attract buyers—it directly contributes to your home’s perceived and real value. Eco-conscious buyers often make faster offers and are more willing to meet or exceed asking prices for homes that promise lower utility costs and environmental responsibility.

Your Next Steps to a Greener, More Valuable Home

Ready to future-proof your home for sustainability-focused buyers? Start with these upgrades:

Replace HVAC systems with energy-efficient models. Invest in ENERGY STAR appliances. Improve insulation through windows, doors, and siding. Swap old bulbs for energy-efficient lighting.

Consult a local real estate expert who understands the growing demand for eco-friendly features in your specific market. Let’s connect and create a strategy that positions your home as a top choice for eco-conscious buyers!

Discover how less clutter and simple staging strategies can increase your home’s market value and attract buyers fast.

Clean, staged living space highlighting less clutter and more value when selling your home.

First Impressions Sell Homes

First impressions truly matter—especially when you’re trying to sell your home. In today’s real estate market, buyers make snap decisions based on initial visuals. Walking into a messy, overcrowded house can be distracting, preventing potential buyers from seeing the property’s real potential. The good news? A well-staged home, as illustrated in the image above, doesn’t need expensive upgrades. Minimalism, smart furniture placement, and neutral tones can boost perceived value, minimize distractions, and help buyers envision themselves in the space.

Why Less Clutter Equals More Value

According to industry leaders like NAR, staging your home with a minimalist approach creates a blank canvas that appeals to most buyers. A tidy, open space automatically feels more spacious and inviting. This simplicity allows buyers to focus on the home’s best features—be it natural light, quality flooring, or thoughtful layouts.

Simple additions such as neutral pillows, accent tables, or fresh plants (as shown in the photo) can subtly draw attention to the property’s advantages without overwhelming visitors. By depersonalizing and decluttering, sellers help buyers picture their future home.

Simple Steps to Stage for Success

Start Neutral: Use soft, neutral colors for walls and accessories. Maximize Lighting: Open blinds, use daylight bulbs, and position lamps strategically. Smart Layouts: Avoid overfilling rooms. Highlight space by choosing streamlined furniture arrangements. Add Natural Touches: Green plants or tasteful vases bring life without adding clutter. Depersonalize: Store away personal photos or bold décor.

Connecting for Expert Guidance

Thinking about listing your home? Proper staging doesn’t have to be overwhelming. As a real estate professional, I specialize in guiding homeowners like you through the process, creating a tailored plan that maximizes value and minimizes time on the market.

Ready to make your home market-ready? Contact me today for personalized home-staging advice that sells!

Thinking about renting vs buying? Discover why homeownership builds equity, adds stability, and gives you full creative freedom.

Renting vs Buying: A clear comparison to help you choose wisely.

Thinking About Making the Leap from Renting to Owning?

Dreaming of owning your own place? Let’s be honest: deciding whether to rent or buy isn’t always easy. But knowing the real differences can help you make the best move for your future. Today’s housing market might feel intimidating, but the truth is—homeownership often brings long-term rewards renting simply can’t match.

Why Renting Keeps You Limited

No Equity: Paying Without Ownership

Every rent check you send builds your landlord’s wealth—not yours. Renting doesn’t contribute to ownership, leaving you with nothing to show for years of payments.

Rent Increases: Market-Controlled Costs

Leases end. Prices rise. Whether it’s due to market trends or your landlord’s decision, rent increases can hit when you least expect them, squeezing your monthly budget.

Limited Personalization: No Creative Freedom

Dreaming of customizing your kitchen or painting the living room your favorite color? With renting, you’re typically stuck following strict rules, limiting how you personalize your space.

Less Stability: Short-Term Living

Leases are temporary. A landlord’s decision to sell or end the lease could force an unexpected move, adding uncertainty to your housing situation.

No Tax Benefits: Missed Financial Opportunities

Unlike homeowners, renters don’t get tax deductions. Without mortgage interest or property tax deductions, renting often means missing out on financial perks.

5 Key Advantages of Buying a Home

Build Equity: Invest in Your Future

Monthly mortgage payments directly contribute to your ownership. Over time, your home’s value typically grows—building your wealth through equity.

Stability: No Surprise Price Hikes

With fixed-rate mortgages, your payment remains predictable, giving you budget certainty. Say goodbye to unexpected rent increases.

Creative Freedom: Make It Truly Yours

From painting walls to remodeling bathrooms, homeownership gives you full creative control. Finally, design your dream home without asking for permission.

Tax Benefits: Deductions That Pay

Homeowners may qualify for significant tax deductions, including mortgage interest and property taxes. These benefits can save you thousands annually.

Long-Term Investment: Appreciation Potential

Unlike rent payments that vanish monthly, owning offers the chance for home value appreciation, growing your investment over the years.

Renting vs Buying: Which One Fits Your Life Goals?

At first glance, renting may seem simpler—but it’s often a short-term solution. Buying, while requiring commitment, builds your financial foundation. Consider your long-term goals: do you want stability, equity, and control over your space? If so, buying could be your smartest move.

Next Steps Toward Homeownership

From choosing the right neighborhood to securing the best mortgage, navigating your first home purchase can feel overwhelming. But you’re not alone—I’m here to help. Whether you’re comparing rates, reviewing properties, or negotiating offers, let me guide you step-by-step.

Ready to stop renting and start owning? 📲 Message me today to begin your homeownership journey.

FAQs About Renting vs Buying

Is it smarter to rent or buy in 2025?

While renting offers flexibility, buying builds long-term wealth through equity and property appreciation.

What are the risks of buying a home?

Homeownership includes responsibilities like maintenance costs, property taxes, and potential market fluctuations.

How does building equity work?

Equity is the portion of your home you truly own, increasing as you pay down your mortgage and your home’s value rises.

Are there tax breaks for homeowners?

Yes! Homeowners may deduct mortgage interest, property taxes, and sometimes mortgage insurance premiums.

Why is renting sometimes better?

For those needing short-term flexibility or avoiding maintenance costs, renting can make sense temporarily.

How long should I stay in a home to make buying worth it?

Generally, staying five years or more allows your home’s appreciation to offset buying and selling costs.

Conclusion: Why Buying Beats Renting

While renting might feel convenient now, owning a home creates lasting benefits—building equity, providing stability, and offering total creative freedom. Plus, homeowners enjoy tax benefits and long-term investment growth. If you’re dreaming of your own space, it’s time to explore buying.

A seller’s counteroffer means they’re still interested—just with some changes. Learn how to handle counteroffers like a pro.

The seller said “not quite”? That’s your cue to keep talking—counteroffers mean the conversation isn’t over!

Making an Offer Is Only the Beginning

In the world of real estate, making an offer on a home can feel like a giant leap toward your dream home. But what if the seller doesn’t accept right away? Don’t worry—it doesn’t mean it’s over. Instead, they may come back with a counteroffer. That’s not a closed door—it’s a nudge to keep the conversation going.

A counteroffer means the seller saw potential in your offer but had a few tweaks in mind—like the price, closing date, or certain contingencies. This is where savvy negotiation kicks in. It’s not about winners and losers; it’s about finding terms that work for both sides.

What Is a Counteroffer in Real Estate?

A counteroffer is a formal response to your offer, typically suggesting revised terms. The seller might want a higher price, a different closing timeline, or might not agree to covering certain repairs. Your initial offer served as the opening bid. Now, the negotiation dance begins.

Why You Should Welcome a Counteroffer

While it may feel like a hurdle, a counteroffer is actually a green light. It signals that the seller is engaged and motivated to work out a deal—they’re just not quite ready to accept your original terms. This keeps the dialogue going and the door open.

Your Next Steps After a Counteroffer

Review the new terms carefully Consult your real estate agent about negotiation strategy Respond promptly—time is often of the essence Decide whether to accept, reject, or counter back

Being flexible while staying true to your goals is the key. Remember, the goal is a fair deal that satisfies both buyer and seller.

From Offer to Ownership: You’re Not Alone

As your local real estate expert, I’ve guided countless clients through this exact process. From writing the first offer to reviewing counteroffers and sealing the deal, I’m here for every step. If you’re thinking about buying a home, now is the perfect time to reach out.

Let’s turn that “not quite” into a “yes!” Ready to start house hunting? Let’s chat now and make your dream home a reality.

Explore the verified events behind the USA Declaration of Independence, focusing on British economic control and westward expansion limits.

A close-up of a lit sparkler glowing brightly against the backdrop of an American flag, with warm golden bokeh lights in the background—symbolizing Fourth of July celebrations and the spirit of American independence.

The USA Declaration of Independence wasn’t simply a passionate cry for freedom. Behind the rhetoric and ideals lay deeply rooted political frustrations, economic grievances, and imperial constraints—especially the King’s refusal to allow westward expansion after the French and Indian War. This strategic limitation wasn’t merely about maintaining peace; it struck directly at the ambitions of colonial elites and settlers alike.

The USA Declaration of Independence

On July 4, 1776, representatives of thirteen British colonies in North America ratified a declaration that forever changed the world. This bold document severed political ties with Great Britain and established the United States as an independent nation. But its inception was not spontaneous. It was born of escalating conflict between British authority and colonial resistance—fueled not only by taxes and tyranny but by land, profit, and power.

Proclamation of 1763: The Invisible Line That Sparked Rebellion

Following Britain’s triumph in the French and Indian War (1754–1763), King George III issued the Royal Proclamation of 1763, a decree that forbade colonial expansion west of the Appalachian Mountains. Though framed as a peacekeeping measure with Native tribes, colonists saw it as a betrayal.

Why? Because many wealthy Americans—including men like George Washington—had investments in western lands. They anticipated profits from post-war settlement and development. When the Crown drew an invisible line through the Appalachians, it essentially nullified their ventures and blocked access to fertile, lucrative territory.

This move outraged settlers and land speculators, revealing a stark divide between imperial interests and colonial ambition. Many viewed it as an overreach of royal authority that favored British control over colonial prosperity. The restriction not only limited individual dreams but challenged the very concept of American self-determination.

Taxation Without Representation: The Money Grab That Backfired

As if restricting land wasn’t enough, the British government imposed a series of taxes to offset war debt. The Stamp Act of 1765 was the first direct tax, requiring colonists to pay for an official stamp on printed materials. It was met with uproar.

Then came the Townshend Acts (1767), targeting imports like glass, paint, and tea. The colonists saw these as blatant attempts to siphon wealth from the New World. In their view, Parliament had no right to impose taxes without colonial representation.

This resistance wasn’t just populist—it was strategic. Influential leaders, such as Samuel Adams and John Hancock, recognized that financial control equated to political control. The outcry over taxation became a powerful rallying cry across the colonies.

Boston Massacre: A Bloody Turning Point

Tensions boiled over on March 5, 1770, when British soldiers opened fire on a crowd of colonists, killing five men in what would become known as the Boston Massacre. Though the event was sensationalized by propagandists like Paul Revere, the violence underscored the reality of colonial oppression.

The massacre became a symbol of tyranny and helped unify colonial opinion against British occupation. It exposed the costs of protest and deepened the ideological divide between the Crown and its subjects.

Boston Tea Party and the Intolerable Acts

When Parliament passed the Tea Act of 1773, giving the East India Company a monopoly on American tea sales, it triggered one of the most iconic acts of resistance—the Boston Tea Party. On December 16, 1773, colonists disguised as Mohawk Indians dumped 342 chests of tea into Boston Harbor.

In response, the British issued the Intolerable Acts (1774), punitive measures that closed Boston Harbor and dissolved Massachusetts’ self-government. These acts didn’t just punish Boston—they shocked all thirteen colonies into greater unity and fueled calls for a continental congress.

Olive Branch Petition: Last Hope for Peace

Despite rising hostilities, some leaders still sought peace. The Olive Branch Petition, sent in July 1775, was a final appeal to King George III to prevent war. He rejected it outright and declared the colonies in rebellion. This dismissal destroyed any remaining hope of reconciliation and confirmed for many that independence was the only viable path.

The Lee Resolution: A Formal Push for Freedom

On June 7, 1776, Richard Henry Lee introduced a motion in the Second Continental Congress: that the colonies “are, and of right ought to be, free and independent States.” This marked the formal beginning of the process that would lead to the USA Declaration of Independence.

Though hotly debated, the resolution passed on July 2, 1776. The document that followed—primarily drafted by Thomas Jefferson—was adopted two days later.

Jefferson’s Declaration and Its Redacted Truths

Jefferson’s original draft included a scathing indictment of slavery and the British Crown’s role in it. But to maintain unity among southern colonies, those passages were removed. It was a compromise that reflected the complex interplay between idealism and self-interest that characterized the Revolution.

Chronological Summary of Key Events

Date Event

1763

Royal Proclamation restricts westward expansion

1765

Stamp Act incites mass protest

1770

Boston Massacre ignites outrage

1773

Boston Tea Party deepens conflict

1774

Intolerable Acts punish Massachusetts

1775

Olive Branch Petition rejected

1776

Lee Resolution and Declaration of Independence adopted

Myths vs. Historical Reality

Myth: All colonists yearned for liberty. Truth: Many colonists, including Loyalists, opposed independence. Myth: The Declaration was signed on July 4. Truth: Most delegates signed on August 2, 1776. Myth: The war was purely ideological. Truth: It was also about economics, land, and political power.

Lasting Impact of the Declaration

The USA Declaration of Independence didn’t just announce a break from Britain—it inspired revolutionary movements across the globe. Its language on liberty and human rights remains a beacon, though its compromises still echo in American politics today.

This summer, take the stress out of house hunting. Find the right real estate agent and build your dream team with expert connections you can trust.

Sizzlin’ Summer Tip: The right agent makes all the difference. Let me help you find the dream team to get you home faster!

The right agent makes all the difference—and here’s why it matters more than ever.

Buying a home is one of the biggest decisions you’ll ever make, and let’s be honest—it can feel downright overwhelming at times. But there’s good news! You don’t have to go it alone. In fact, the right real estate agent can transform the process from stressful to smooth sailing. Whether it’s negotiating a great deal or spotting red flags before they become roadblocks, your agent is your guide, advocate, and teammate every step of the way.

So how do you find that perfect fit?

Let’s dive into the key reasons why the right agent—and the right team—makes all the difference.

Why the Right Agent is the Secret Ingredient

Think of your homebuying journey like a summer barbecue. You wouldn’t throw a steak on the grill without making sure it’s seasoned to perfection, right? In the same way, your real estate transaction needs the right mix of expertise, communication, and trust to really sizzle.

An experienced, local-savvy agent will:

Understand your goals and priorities Provide insight into the neighborhood and market Spot potential issues with properties Connect you with trusted mortgage lenders, inspectors, and more

That’s why my network = your dream team.

Your Dream Team Starts Here

As a mortgage loan officer, I’ve partnered with some of the best real estate professionals in the business. These are people I trust to go the extra mile—because that’s exactly what I do for you.

I’ll help you:

Match with a top-tier agent tailored to your needs Simplify the mortgage process from start to finish Build a homebuying team that works together seamlessly

🔑 The key to a smooth experience is working with people who care.

Let’s Make Home Happen—Together

There’s no need to tackle the market on your own. With my connections and guidance, your dream of homeownership becomes a reality—faster and with fewer headaches.

We all obsess over dream homes online, but before your heart gets set, getting pre-approved for your mortgage can make all the difference. Learn how to empower your homebuying journey with this guide.

Don’t just dream—get pre-approved before you fall in love with houses online.

Why This Meme Hits Every Homebuyer Right in the Feels

We’ve all been there. Sitting on the couch, scrolling through listings on Zillow or Realtor.com late at night, imagining ourselves sipping coffee in that bright kitchen or lounging on that oversized porch.

This viral meme nails it:

“I want someone to look at me the way we all look at houses online.”

But here’s the reality check: Falling in love with a house before getting pre-approved for your mortgage can be a setup for heartbreak.

Before your heart runs wild, let’s talk about why getting pre-approved needs to be your very first step.

Educate: What Does Pre-Approval Really Mean?

Mortgage pre-approval is a lender’s way of saying, “Yes, we’re ready to back you up—up to this specific amount.” It’s based on a detailed review of your credit score, income, employment, and assets.

Without pre-approval, you’re shopping blind.

Some key benefits of getting pre-approved:

Know your budget: No more guessing games. Gain negotiation power: Sellers take you seriously. Speed up the closing process: Less paperwork stress later.

According to The Consumer Financial Protection Bureau, buyers who get pre-approved have a stronger chance of getting their offers accepted, especially in competitive markets.

Empower: Why You Deserve to Shop Smart

You wouldn’t walk into a store with no wallet and expect to check out, right?

The same goes for home shopping. Empower yourself by getting your financial house in order before you fall for a house online.

Here’s how pre-approval puts you in control:

You’ll scroll with confidence: Knowing exactly what you can afford. You’ll avoid emotional rollercoasters: No more heartbreak over homes out of budget. You’ll be offer-ready: The minute you find “the one,” you’re ready to pounce.

Execute: Actionable Steps to Get Pre-Approved Fast

So how do you get pre-approved without overthinking it?

Gather your documents: Pay stubs, W-2s, bank statements, and tax returns. Check your credit: Know your score and work on improving it if needed. Contact a trusted mortgage lender: Someone like the experts at TeamMortgageMack can walk you through the process. Discuss loan options: Fixed rate, FHA, VA… make sure you choose what fits. Get your pre-approval letter: Now you’re ready to shop with confidence.

Pro Tip: Want to avoid delays? Stay responsive during the underwriting process and avoid big financial moves (like buying a car) while you’re house hunting.

Experience: Enjoy the Online Home Shopping Journey Without Regret

Once you’re pre-approved, browsing online listings becomes so much more exciting. You’re no longer dreaming—you’re shopping with real buying power.

That charming bungalow or that ultra-modern condo isn’t just a fantasy anymore. It’s within reach.

Plus, sellers will know you’re a serious buyer. In multiple-offer situations, a pre-approved offer often rises to the top.

Want more tips on turning dreams into keys in your hand? Explore more E4 (Educate, Empower, Execute, Experience) homebuying strategies on TeamMortgageMack.com.

Not sure where to start when choosing a real estate agent? You’re not alone! Most home buyers rely on referrals to find the perfect agent. Here’s why referrals work—and how I can help connect you with the right professional.

Text conversation graphic showing how referrals help connect home buyers with trusted real estate agents. Source: NAR Home Buyers and Sellers Generational Trends Report, via ListReports 2025.

If you’re not sure where to start with finding a real estate agent, I’ve got you covered! 🤝 The home-buying process can feel overwhelming, but here’s the good news: you don’t have to figure it out alone.

According to the NAR Home Buyers and Sellers Generational Trends Report, the number one way home buyers find their real estate agent is through referrals from friends, family, or trusted professionals.

🏡 Why Referrals Work So Well in Real Estate

Choosing a real estate agent is personal. You need someone who understands your goals, your budget, and your timeline. Referrals come with built-in trust and social proof. When someone you know has had a great experience, you’re more likely to feel confident working with that agent.

Here’s why referrals are powerful:

✅ You get firsthand insight into the agent’s work style. ✅ You know the agent has a proven track record. ✅ You save time researching countless online profiles.

🤔 Don’t Know Anyone in Real Estate? That’s Where I Come In!

I work with trusted, experienced agents every day. Whether you’re buying your first home, upsizing, or relocating, I can help you find the perfect match for your needs and personality.

The right real estate team can make all the difference between a stressful process and a smooth, exciting journey to your dream home.

Explore the historical timeline that led to the celebration of Juneteenth as a national holiday. Honor the legacy of freedom, equality, and the continued fight for justice.

Today we honor the journey toward freedom, equality, and justice while remembering that the work continues daily. Happy Juneteenth.

The Long Road to Freedom: The Chronology of Juneteenth

The origins of Juneteenth trace back to the final chapters of slavery in the United States. On January 1, 1863, President Abraham Lincoln issued the Emancipation Proclamation, declaring “that all persons held as slaves” within the rebellious states “are, and henceforward shall be free.” Yet, freedom was not immediate for all.

In Texas, which was far from the Union stronghold, slavery persisted for more than two years after this declaration. It wasn’t until June 19, 1865, that Union General Gordon Granger arrived in Galveston, Texas, and read aloud General Order No. 3, officially freeing the last remaining enslaved African Americans.

That pivotal day became Juneteenth, a portmanteau of “June” and “nineteenth,” and marked the true end of slavery in the United States.

However, Juneteenth did not become a national celebration overnight. In the immediate years following 1865, African American communities began commemorating the day with gatherings, music, prayer, and the reading of the Emancipation Proclamation. Over time, Juneteenth grew in cultural significance, especially in Southern states like Texas, Louisiana, and Arkansas.

Yet, systemic racism and segregation pushed Juneteenth celebrations into church yards and rural areas during the Jim Crow era. Despite this, Black communities kept the tradition alive through barbecues, parades, and family reunions, turning Juneteenth into a vibrant annual symbol of perseverance.

Fast forward to 1980, when Texas became the first U.S. state to declare Juneteenth an official state holiday. Gradually, other states followed. But national recognition remained elusive—until tragedy sparked renewed urgency.

The murder of George Floyd in 2020 catalyzed a racial reckoning across the country. Protesters and educators alike demanded systemic change, and Juneteenth reemerged as a powerful emblem of unfulfilled promises. In June 2021, momentum reached the highest levels of government when President Joe Biden signed the Juneteenth National Independence Day Act into law, making it the 11th federal holiday in the United States.

Today, Juneteenth is not just a Black holiday; it’s an American holiday—a chance for all people to reflect on freedom, equality, and justice. From grassroots activism to federal legislation, Juneteenth’s journey is proof that change is possible—even when it takes 156 years.

Juneteenth History Uncovered: The 156-Year Journey to a National Holiday

The Long Road to Freedom: The Chronology of Juneteenth

1863

Emancipation Proclamation: A Promise of Freedom

1865

Galveston and General Granger: Juneteenth is Born

Reconstruction

Juneteenth in the Reconstruction Era

Early Celebrations

Jim Crow Laws and the Hidden Legacy of Juneteenth

20th Century

Community Resistance and the Power of Black Tradition

1980 Onward

Texas Leads the Way: The First Official State Holiday

Cultural Revival

Music, Food, and Prayer: The Soul of Juneteenth

2020 Catalyst

George Floyd and the Modern Civil Rights Awakening

2021 Milestone

Juneteenth Becomes a National Holiday

FAQs

What is Juneteenth and why is it important?

Juneteenth marks the date enslaved people in Texas were finally informed of their freedom in 1865, two years after the Emancipation Proclamation.

Is Juneteenth a national holiday now?

Yes, as of June 17, 2021, Juneteenth is officially recognized as a U.S. federal holiday.

How do people celebrate Juneteenth?

Common activities include parades, festivals, prayer services, historical reenactments, and family gatherings with soul food and music.

Why did it take so long for Juneteenth to become a national holiday?

Systemic racism, political indifference, and a lack of national awareness delayed federal recognition until recent years.

How can I honor Juneteenth in my community?

Attend events, support Black-owned businesses, educate others about its history, and advocate for racial justice policies.

What does Juneteenth teach us today?

Juneteenth is a powerful reminder that freedom is not given but fought for—and that justice delayed is justice denied.

A real estate counteroffer can feel intimidating, but it’s a common part of the home buying process. Here’s how to respond strategically and smartly.

Navigating the art of real estate counteroffers is key to securing your dream home.

Understanding the Real Estate Counteroffer Process

In real estate, a counteroffer is when a seller doesn’t fully accept a buyer’s offer and proposes changes. These tweaks may include the price, closing date, contingencies, or other terms. Rather than viewing this as a rejection, see it as the start of a negotiation. After all, this “dance” is common and crucial for both parties to feel satisfied with the final agreement.

Why Counteroffers Are Common in Home Buying

Sellers make counteroffers to reflect their priorities—whether that’s a higher price, fewer contingencies, or a specific timeline. For buyers, this step signals interest, not dismissal. A counteroffer means the seller is open to negotiating, which is good news for you.

Key Tips for Handling a Real Estate Counteroffer

Respond Quickly, But Thoughtfully

Timing is essential. Sellers often include an expiration date on their counteroffer. Responding quickly keeps negotiations active, but take time to assess the terms. Consult your real estate agent, who will provide insights on what’s reasonable in your market.

Understand What’s Being Changed

Don’t rush through the document. Look closely at the price, contingencies (like inspections or financing), dates, and included items (like appliances or fixtures). Even minor changes can affect your deal and your wallet.

Know When to Compromise and When to Walk

You don’t have to accept every term, but know which points matter most to you. Are you okay with a slightly higher price if it includes closing cost assistance? Or is the inspection contingency a non-negotiable? Your agent can help you evaluate the big picture.

Put Everything in Writing

Verbal agreements don’t count in real estate. Ensure all terms—no matter how minor—are clearly documented. This avoids misunderstandings and legal troubles down the line.

Lean on Your Agent’s Expertise

A good real estate agent isn’t just there to open doors—they’re your negotiator, guide, and advocate. Let them handle communications and strategize your counteroffer. With their experience, you’re in better hands.

What Happens After a Counteroffer Is Accepted?

Once both parties agree on the terms, the purchase agreement becomes binding. At this point, the process moves into inspections, financing, and preparing for closing. That’s when your dream home truly becomes yours.

FAQs About Real Estate Counteroffers

What is a counteroffer in real estate?

A counteroffer is a seller’s response to a buyer’s offer with adjusted terms like price or conditions. It keeps negotiations open.

Can a buyer reject a counteroffer?

Absolutely. A buyer can accept, reject, or issue another counteroffer. It’s a back-and-forth process.

How long does a counteroffer last?

Most counteroffers include an expiration—often 24 to 72 hours. If not accepted in time, the offer becomes void.

Do I need a real estate agent for counteroffers?

While not mandatory, having an agent is highly recommended. They understand market conditions and how to negotiate effectively.

Can you make multiple counteroffers?

Yes, both buyers and sellers can go back and forth with offers and counteroffers until a mutual agreement is reached—or negotiations end.

What should I do if I feel overwhelmed?

Take a breath. Lean on your agent. They’ve navigated dozens of negotiations and can guide you calmly through the chaos.

Ready to Navigate the Real Estate Market?

A counteroffer doesn’t have to be intimidating. It’s a sign that you’re on the path to a deal. Stay calm, work with a seasoned agent, and keep your eyes on the ultimate prize—a place to call home.

Upgrading your kitchen is a smart move that adds joy and value—perfect for homeowners looking to sell soon or simply improve their space.

Freshly renovated kitchen with modern finishes—a top value-boosting upgrade for sellers.

Thinking about upgrading your kitchen? Whether you’re preparing to sell or planning for a future move, investing in a kitchen refresh is a strategic decision with lasting benefits. Not only does a modernized kitchen enhance daily living, but it also adds significant resale value—a true win-win for any homeowner.

Boosting Value Through Smart Renovations

Modern buyers expect clean, functional, and stylish kitchens. Outdated countertops or dim lighting can be deal-breakers. Instead, focus on sleek finishes, open shelving, energy-efficient appliances, and durable flooring to appeal to a broader market.

The Emotional ROI of Kitchen Remodels

Sure, the return on investment is great—but let’s not underestimate the emotional return. Picture yourself sipping coffee in a fresh, sunlit space or preparing dinner with upgraded appliances. A revitalized kitchen enhances quality of life now while preparing for future returns.

Best Kitchen Upgrades That Attract Buyers

Quartz or granite countertops: Durable and luxurious

Updated cabinets: Shaker-style or flat-panel are trending

If you’re planning to list soon, now’s the time. Even if a move is a few years off, incremental upgrades can make the process smoother and budget-friendly. Start small and build toward a fully refreshed kitchen by listing day.

Budgeting Tips for a Kitchen Upgrade

Set priorities: Focus on what offers the highest ROI.

DIY where possible: Painting cabinets or installing a backsplash can save you hundreds.

Work with a pro: Consulting a real estate-savvy contractor ensures your updates align with market expectations.

According to the 2024 Cost vs. Value Report, minor kitchen remodels often yield higher ROI than upscale overhauls.

Want Help Deciding What’s Worth It?

Not sure whether to replace your cabinets or simply refinish them? That’s where a local expert comes in. Real estate professionals know what features matter most in your area. Reach out for guidance tailored to your home and neighborhood.

Don’t search solo! Discover how having a real estate pro helps you find your dream home faster and smarter. Skip the stress and get expert help.

Your dream home is closer than you think—let a pro guide the way.

Searching for your dream home can feel like chasing a moving target in a crowded field. Why spend precious time searching solo when you could have a pro in your corner from the start? Whether you’re browsing listings on your lunch break or gearing up to make an offer, having a real estate expert by your side can be the key to unlocking your perfect space faster, smarter, and with fewer regrets.

Let’s be real—this journey isn’t just about open houses and Pinterest boards. It’s contracts, negotiations, inspections, and strategy. Here’s how teaming up with a pro (that’s me! 👋) changes the game from day one.

Why You Need Help with House Hunting

Looking for a home isn’t like ordering shoes online. You’re dealing with the largest purchase of your life. And mistakes? They can be costly—financially and emotionally. From market trends to hidden neighborhood gems, an experienced agent brings inside info you can’t get from Zillow.

Avoid Costly Mistakes and Pitfalls

A professional knows what to look out for. Is that adorable fixer-upper really a money pit in disguise? Will that new condo be worth more next year, or are there signs of overpricing? The right agent helps you read between the lines and avoid emotional decisions that hurt later.

Speed Up the Process with Expert Insights

Your time is valuable. With access to off-market listings and real-time alerts, you won’t be stuck in the waiting game. A pro filters options based on your lifestyle, commute, and future plans—so every showing is worth it.

Make Stronger, Smarter Offers

Not sure how much to offer or how to compete in a hot market? Your agent (me!) knows the strategies to stand out without overpaying. I’ll walk you through terms, contingencies, and how to craft an offer sellers take seriously.

It’s Okay If You’re Just Browsing

You don’t have to be ready to buy tomorrow to get help today. A good real estate partner respects your pace and provides value early on—answering questions, showing possibilities, and helping you explore with clarity.

Let’s Team Up: Your Dream Home is Out There

Your next home might already be waiting. So instead of wandering through this process alone, why not tag in a guide who knows the terrain?

DM me today—let’s take the guesswork out of your search and replace it with confidence. I’m not just here for the sale; I’m here to make the whole experience better.

Looking for a home with more room to breathe? Whether it’s expanding your family or finally getting that home office, discover why upsizing your home could be the best move you make this year.

A beautiful home exterior with a “For Sale” sign, representing the excitement of upsizing for a better lifestyle.

Sometimes You Just Need a Little More Room

Life evolves—and with it, so do our space needs. Maybe your family is growing, your hobbies are expanding, or perhaps you’re simply yearning for a dedicated workspace where you can focus without distractions. That’s where the idea of upsizing comes in.

Upsizing your home isn’t about extravagance—it’s about aligning your environment with your lifestyle. As a knowledgeable real estate professional, I understand how space—or the lack of it—can impact your quality of life. That’s why I’m here to help guide you through the process, from deciding to move to finding the perfect fit that matches both your lifestyle and your budget.

More Space, More Possibilities

With a larger home, you gain more than square footage—you gain flexibility. Imagine turning that extra room into a home gym, a quiet reading nook, or a vibrant playroom for the kids. The possibilities are endless, and the benefits are profound:

Family Growth: Growing families often need more bedrooms and bathrooms.

Work From Home: A home office is essential in today’s flexible work landscape.

Entertaining Guests: More space allows for better hosting and hospitality.

Future Planning: Buying bigger today may reduce the need for another move tomorrow.

Increased Property Value: Larger homes in good locations often appreciate faster.

Navigating the Buying Process with Confidence

The thought of buying a bigger home might feel overwhelming, but you’re not alone in this journey. I offer tailored support to ensure you’re confident at every step:

Budget Planning: We’ll match your needs with your financial situation. Neighborhood Insights: I’ll help you find communities that offer space and value. Property Comparisons: We’ll review properties to ensure the best fit. Step-by-Step Guidance: From mortgage pre-approval to closing day, I’ve got you covered.

Ready to Explore Your Options?

There’s no better time than now to discover what upsizing can offer. Your dream home isn’t just about more space—it’s about a better lifestyle, more comfort, and a home that evolves with you.

Let’s chat about what you need, what you want, and how we can find the perfect property that gives you both.

Even after you’re pre-approved, your home loan isn’t guaranteed. Learn which financial mistakes can delay—or cancel—your mortgage approval right before closing day.

Don’t let last-minute financial decisions ruin your home loan—know what not to do before closing.

Buying a home is an exciting milestone, but it’s also one of the most delicate financial processes you’ll ever go through. Once you’re under contract and heading toward closing day, it might feel like you’re in the clear—but you’re not there yet.

Certain financial decisions can jeopardize your loan approval, even in the final hours. Let’s walk through what you should absolutely avoid doing before closing on your home loan.

Why the Closing Period Matters So Much

The time between getting pre-approved and the actual closing is critical. Lenders continue to monitor your financial behavior during this period. That means even small changes to your credit, income, or debt could delay or completely derail your home purchase.

Financial Mistakes That Could Cost You Your Home

You might be surprised to learn how easy it is to mess up a home loan approval. Here are the biggest mistakes to avoid:

1. Opening New Credit Cards

That store credit card might come with tempting discounts, but it can also trigger a drop in your credit score or raise your debt-to-income ratio. Even a seemingly harmless card can signal to your lender that you’re taking on new financial risks.

2. Making Large Purchases

Hold off on buying furniture, appliances, or even a new TV until after you close. Large purchases—especially those made on credit—can add debt, change your financial standing, and send warning signals to lenders.

3. Taking Out a Personal Loan

This is a big one. A personal loan, whether for a wedding, vacation, or other expenses, introduces new debt into your profile. This could lead to delays or even cause your mortgage to be denied.

4. Changing Jobs

Switching employers can create instability in your employment history, even if the new job pays better. If your income structure or job type changes (e.g., from salaried to contract), your lender may need to re-verify your income and employment, which could cause delays.

5. Missing a Bill Payment

Timely payments are crucial during this phase. A missed payment can lower your credit score and raise red flags for your lender. Stay current on all accounts—credit cards, utilities, auto loans, and more.

Why These Mistakes Matter to Lenders

Lenders approve your mortgage based on the snapshot of your financial health at the time of pre-approval. If that picture changes, even slightly, your loan could be reevaluated. These last-minute changes could mean higher interest rates, added loan conditions, or complete denial.

Pre-Approval Isn’t a Green Light—It’s a Caution Sign

Many buyers assume that pre-approval means their financing is locked in. But lenders will run a final check on your credit and employment just days before closing. Any red flags during this final review can cause a major setback.

How to Protect Your Loan Approval

To stay mortgage-ready through closing, maintain financial consistency. Avoid new debt, don’t apply for credit, and don’t make any drastic lifestyle changes. Keep your financial picture as stable as it was the day you were pre-approved.

When in Doubt—Ask!

If you’re unsure whether a financial move could hurt your mortgage, ask your loan officer or real estate agent first. It’s always better to be safe than to risk losing your dream home over a new credit card or car purchase.

Final Thoughts

Securing a home loan isn’t just about what you do to get approved—it’s also about what you don’t do afterward. The final stretch before closing is not the time for big financial decisions. Your lender is watching, and your future home is on the line.

If you ever have questions about the process, I’m just a message away and can connect you with a trusted loan officer to guide you. Let’s make sure your journey to homeownership is smooth and successful.

Discover the top 3 reasons why buying a previously owned home might be your smartest move yet. Better pricing, greater value, and unique charm await!

Top 3 reasons previously owned homes are purchased: Better price, Better overall value, and More charm and character.

There’s Something Special About Previously Owned Homes

There’s something truly magical about stepping into a house that already has a story. Unlike brand-new constructions, previously owned homes offer a unique blend of personality, value, and affordability that simply can’t be duplicated. If you’re considering making the leap into homeownership, a resale property might just be the perfect fit for you!

Top 3 Reasons Buyers Choose Previously Owned Homes

1. Better Price

Buying a previously owned home often means getting a better price compared to new builds. Builders of new properties typically charge a premium for untouched construction, modern designs, and the latest features. On the flip side, resale homes usually come at a more competitive cost, giving buyers more house for their money—and often leaving extra room in the budget for upgrades or personal touches.

2. Better Overall Value

When it comes to the overall package, previously owned homes often deliver unbeatable value. These homes may already come with established landscaping, upgraded appliances, finished basements, or even bonus amenities like sheds or sunrooms. All these extras add incredible worth without the hefty price tag of installing them yourself, maximizing the return on your investment.

3. More Charm and Character

There’s no denying it—many older homes boast charm and character that newer homes simply can’t match. Whether it’s original hardwood floors, intricate crown molding, vintage fireplaces, or architecturally unique layouts, a previously owned home can offer warmth, personality, and a sense of history that transforms a house into a true home.

Ready to Start Your Homeownership Journey?

If the thought of owning a beautiful, character-filled home at a great value excites you, you’re not alone! Finding the right financing partner is your next important step. I’m here to guide you through every step of the process, helping you make your dream of homeownership a reality. Let’s connect and start building your future today!

Learn the essential mistakes to avoid before your home closing day to ensure a smooth, delay-free homeownership journey.

Stay on track for a successful closing by avoiding these financial pitfalls.

Introduction: Navigating the Home Stretch

Buying a home is exciting, especially as you near the finish line. However, it’s crucial to remain cautious. Last-minute mistakes can jeopardize your closing process, potentially causing delays or even disapproval of your loan. Let’s explore some critical actions you should avoid to ensure a smooth closing experience.

Top Mistakes to Avoid Before Closing

When approaching your closing date, maintaining financial consistency and stability is key. Here are essential activities you must steer clear of:

1. Opening New Credit Cards: New credit inquiries can significantly impact your credit score, potentially affecting your loan approval.

2. Making Large Purchases: Purchasing expensive items like furniture or appliances can alter your debt-to-income ratio, which lenders scrutinize closely.

3. Taking Out Personal Loans: New debt obligations can alarm lenders and affect your loan eligibility.

4. Changing Jobs: Stability in employment is crucial for mortgage approval; a sudden change can disrupt the closing process.

5. Missing a Bill Payment: Late or missed payments negatively impact your credit score, creating red flags for lenders.

Keep Your Finances Stable

To avoid disrupting the loan process, maintain your financial practices as steady and predictable as possible. Avoid significant withdrawals or deposits unless absolutely necessary, and always consult your mortgage professional first.

Stay Employed and Reliable

Lenders prefer stability. If a job change is unavoidable, notify your mortgage lender immediately to discuss potential impacts. Ideally, wait until after closing to pursue new employment opportunities.

How a Mortgage Professional Can Help

Feeling unsure? That’s completely normal. Having a knowledgeable loan officer by your side can alleviate stress. As your mortgage professional, I’m here to guide you, answer your questions, and ensure you reach your closing day confidently and smoothly.

Final Thoughts: Close with Confidence

You’re nearly there! Avoiding these common missteps ensures nothing interferes with the exciting moment you get the keys to your dream home. Need clarity or support? Reach out—let’s get you across the finish line without a hitch.

Ready to stretch out? Discover how to make your move to a bigger home—or upgrade your current one—with the right mortgage strategies that match your lifestyle and budget.

Sometimes you just need more space—aka, more square footage. Whether you’re upsizing or renovating, smart financing makes it possible.

How to Upgrade Your Home with Smart Financing Solutions

It’s not just you—many homeowners and homebuyers are realizing that their current space just doesn’t cut it anymore. Maybe your family’s grown, you’re working from home more, or you simply want a little breathing room (hello, dream kitchen or extra bedroom!). As the image above says, Sometimes you just need space—and in real estate, that usually means more square footage.

But let’s be honest: stretching out can stretch the budget too. That’s where I come in.

Whether you’re looking to purchase a larger home or renovate the one you already love, there are mortgage solutions that can help you make it happen—without the financial stress. From pre-approvals for upsizing to renovation loans that allow you to build out or reconfigure, we’ll align your home goals with your financing strategy.

Financing Options to Consider:

1. Conventional Loans with Higher Limits

Today’s market may offer more flexibility than you think. Let’s review your budget and income to see what you can comfortably afford.

2. Renovation Loans (FHA 203k or Homestyle Loans)

Love your location but need more room? These loan types let you borrow based on the future value of your home post-upgrade.

3. Bridge Loans

Moving before you sell? A short-term solution like a bridge loan might help you make that transition smoother without juggling payments.

Let’s Talk About What Fits

If square footage is your next step, let’s discuss how to make that dream a reality. I’ll guide you through every stage—from loan options to closing—so that expanding your lifestyle doesn’t come with financial overwhelm.

Discover what collateral means in the mortgage world and why your home plays a vital role in securing your loan. Learn how it protects lenders and empowers borrowers.

Understanding collateral: Your home often secures your mortgage loan, giving lenders confidence and offering you better terms.

What Is Collateral?

When it comes to buying a home or securing any type of loan, collateral plays a starring role. But what exactly is it? In simple terms, collateral is an asset that secures a loan—a safeguard for lenders that allows them to recover the money if the borrower defaults.

In the case of a home loan, the collateral is usually the home itself. That means if the borrower is unable to repay the loan, the lender can take possession of the house through foreclosure to recover their funds. While that may sound intimidating, collateral also works in your favor as a borrower—it helps you qualify for better terms, including lower interest rates and higher loan amounts.

Why Is Collateral Important?

Collateral offers security to the lender, but it also demonstrates your commitment as a borrower. When you put up an asset—especially something as significant as a home—you show you’re invested in the transaction. This reduces the lender’s risk, which can result in:

• Lower interest rates

• Flexible loan terms

• Higher chances of approval

• Increased borrowing power

By understanding how collateral functions, homebuyers can make smarter financial decisions and feel more confident when approaching the mortgage process.

What Happens If You Default?

If a borrower fails to make payments on their loan, the lender has the legal right to seize the collateral. This is why it’s crucial to borrow responsibly and work with a trusted loan officer who can guide you to the right loan structure for your financial situation.

Final Thoughts

Collateral isn’t just a technical term—it’s a foundational part of responsible lending and borrowing. Whether you’re buying your first home or refinancing, knowing how collateral works empowers you to make the best choices for your future.

Have questions about collateral or home loans? Let’s connect and talk through your options. Your dream home is closer than you think.

Thinking about buying a home? Prepare like a pro! Learn the 5 essential steps to take before applying for a mortgage to boost your approval chances and save money.

Tips to follow before applying for a mortgage—check your credit, save smart, and prep like a pro!

Buying a home is one of the biggest financial decisions you’ll ever make—and the mortgage application process can feel overwhelming. But with a little upfront planning, you can position yourself for success. Here are five crucial steps to take before you apply for a mortgage.

1. Check Your Credit Score Early

Your credit score is a key factor that lenders evaluate when determining your mortgage eligibility and interest rate. A higher score often means better loan terms.

Action Steps:

• Request your free credit report from all three major bureaus.

• Dispute and resolve any errors or outdated information.

• Pay off any lingering debts or late payments.

2. Avoid Major Purchases

Planning to buy a car or finance new furniture? Wait until after you’ve closed on your home. Major purchases can alter your debt-to-income ratio and reduce your mortgage approval chances.

Tip: Lenders re-check your finances before closing, so hold off on big spending—even if you’re pre-approved.

3. Save for Closing Costs